Keyence Corporation (6861 JT Equity, KYCCF)

The elusive industrial titan of Japan

A brief glance at Keyence’s stock price will leave investors in awe. Keyence is a top-tier cyclical compounder that might arguably be one of the best industrial businesses in the world. With Japanese equities exceeding global investors’ expectations this year, there is now much greater interest in Japanese equities; and I believe this is an opportune time to dive deeper into one of the best businesses in Japan.

This post serves to provide a concise background of the company, market cycle and a perspective on valuation. I won’t delve into the technical details of Keyence’s products as there are probably better resources out there that serve that purpose.

Business description

Keyence is a fabless maker of industrial vision equipment (a.k.a. sensors) and solutions that are used to detect, identify and measure objects. These products have become mission-critical in multiple key end markets (such as the automotive, semiconductors, renewables, healthcare sectors etc.) and are purchased by some 300,000+ customers globally. Some key product categories include:

Sensors — mainly used in defect detection and quality control

Measurement systems & microscopes — mainly used in labs for R&D and detailed inspection

Marking & printing — marking and labelling machines, 3D printing machines etc.

Process control — programmable logic computers (PLCs), servomotors and digital interfaces (i.e., screens for industrial environments)

38% / 21% / 27% of revenues are generated from Japan / US / Asia respectively, with the remaining from Europe and other parts of the world.

Keyence holds the lion’s share of the global industrial vision market with ~25% share, and it mainly competes with SICK AG (10%), Cognex (6%) and Omron (3%). Though these companies sell industrial vision products, due to the large number of SKUs, products are not entirely comparable on an apples-to-apples basis. For example, Cognex’s products are 100% camera-based, while camera-based products only make up ~40% of Keyence’s catalogue.

However, the key difference is sales strategy — Keyence sells its products 100% direct-to-customers, while a substantial amount of its competitors’ sales are made to third-party vendors. This is a crucial difference and I will get to why it is important shortly.

Financials

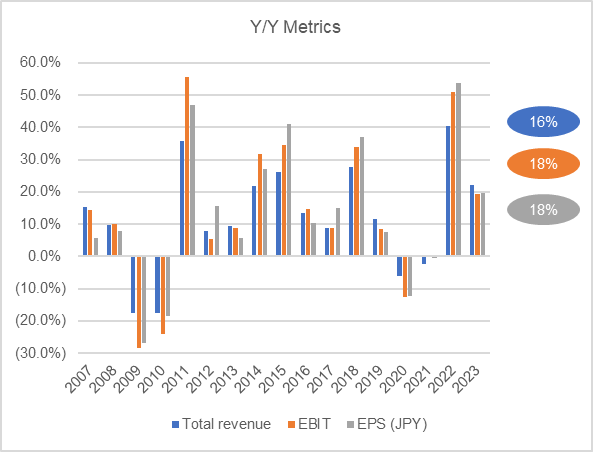

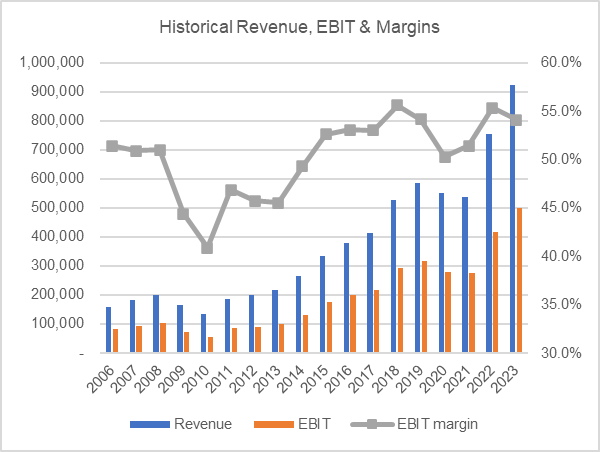

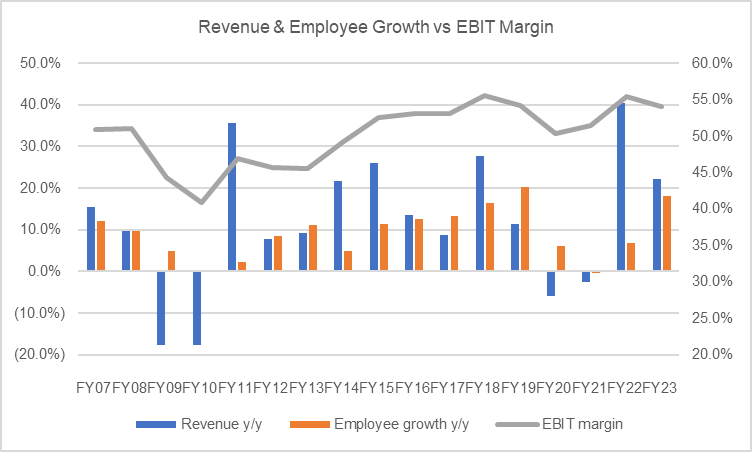

Keyence’s historical financial performance has been nothing short of stellar. The company grew revenues, EBIT and EPS at a CAGR of 16.5%, 17.5% and 18.3% respectively for the past decade.

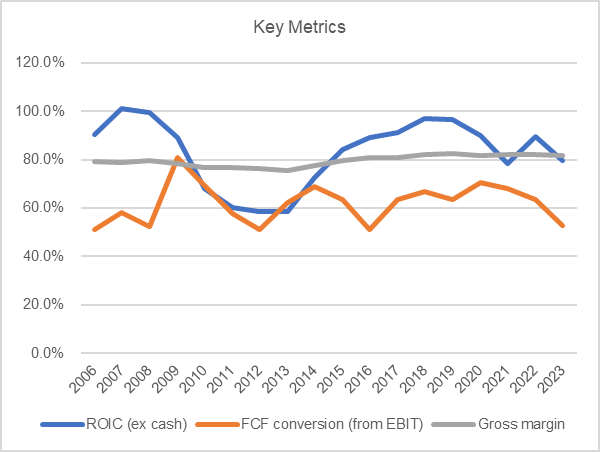

Margins are also phenomenal. >80% gross margin, >50% EBIT margins. Keyence also generates ~80% ROIC, zero debt, a JPY 940bn cash pile; and is highly FCF generative with ~50-60% conversion from EBIT.

High margins can be attributed to a few reasons:

The fabless capital-light model eliminates fixed costs and ensures margin stability during downcycles.

Superior products beget pricing power. Customers are mainly focused on minimizing downtime and saving costs in manufacturing lines. In other words, it doesn’t really matter how much Keyence charges customers for its products, they are willing to spend on high quality products to minimize downtime.

Keyence has a strict “no customization” policy. Standardization further eliminates costs incurred to develop and produce specialized equipment for any one customer. This is unlike Cognex which customizes products for blue chip customers like Apple and Amazon, which make up a combined ~30% of Cognex’s revenues.

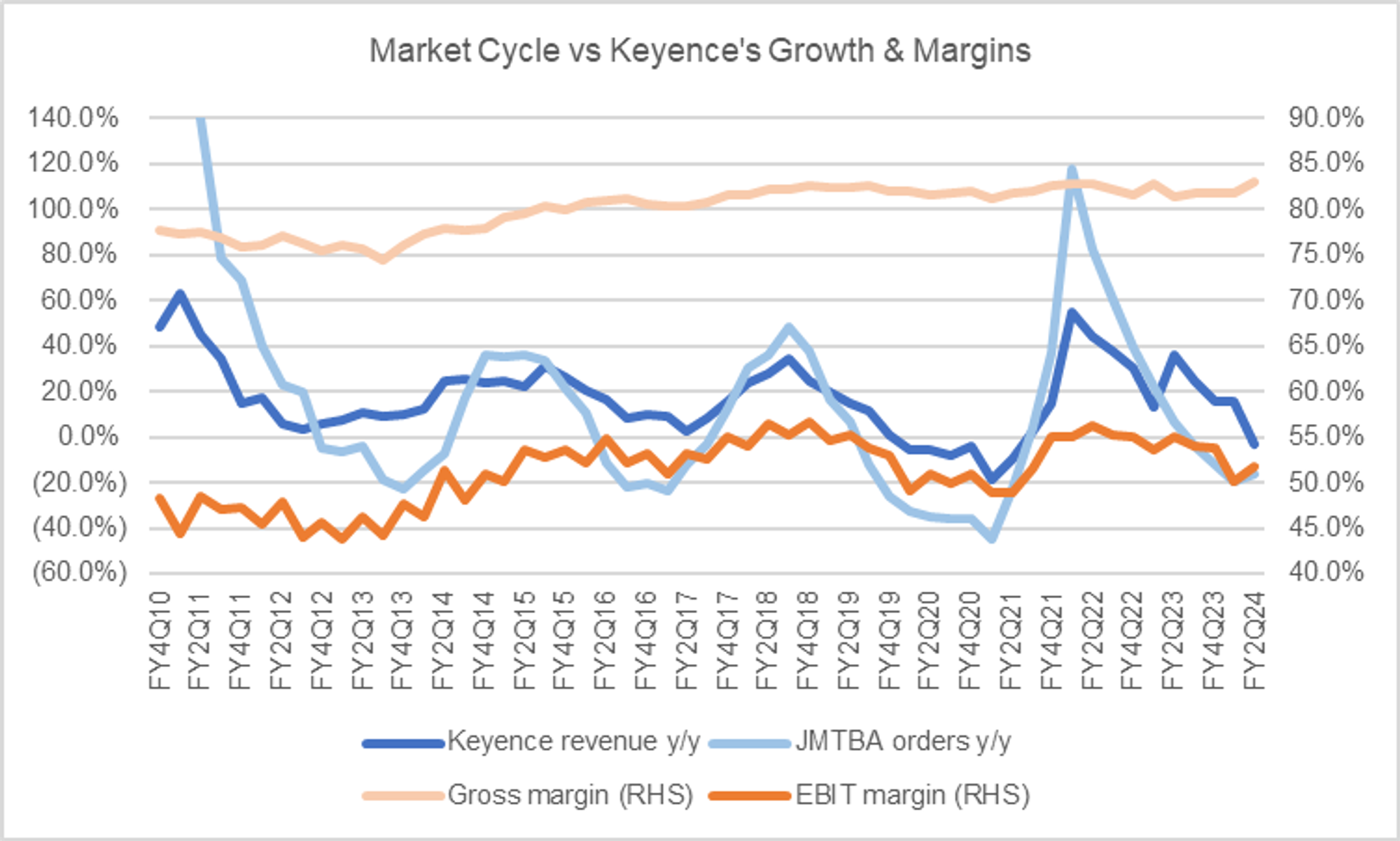

Keyence’s performance during recessions and sector downcycles is equally impressive. Past cycles hardly made any dents in Keyence’s numbers, especially when you compare Keyence with other factory automation (FA) names. In fact, the incredibly resilient gross margins highlighted the firm’s level of pricing power.

However, Keyence’s poor shareholder return is a key concern for many investors. Shareholder return is another issue as the company has been sitting on a huge pile of cash (~70% of total assets) that has not been deployed in M&A or returned to shareholders. Keyence has mentioned that it has always been on the lookout for M&A opportunities (even has an M&A committee inside the management team) but never found the right opportunity. While the lack of shareholder returns might disappoint investors, we can find some consolation in the company’s willingness to deploy cash to bolster growth when the opportunity arises.

A perfectly calibrated business machine

I see Keyence exhibiting the key traits that led to the rise of the best industrial companies (think General Electric during the Jack Welsh era, TransDigm, Danaher, Roper etc.) — laser-focus on (1) operational & product excellence and (2) profitability.

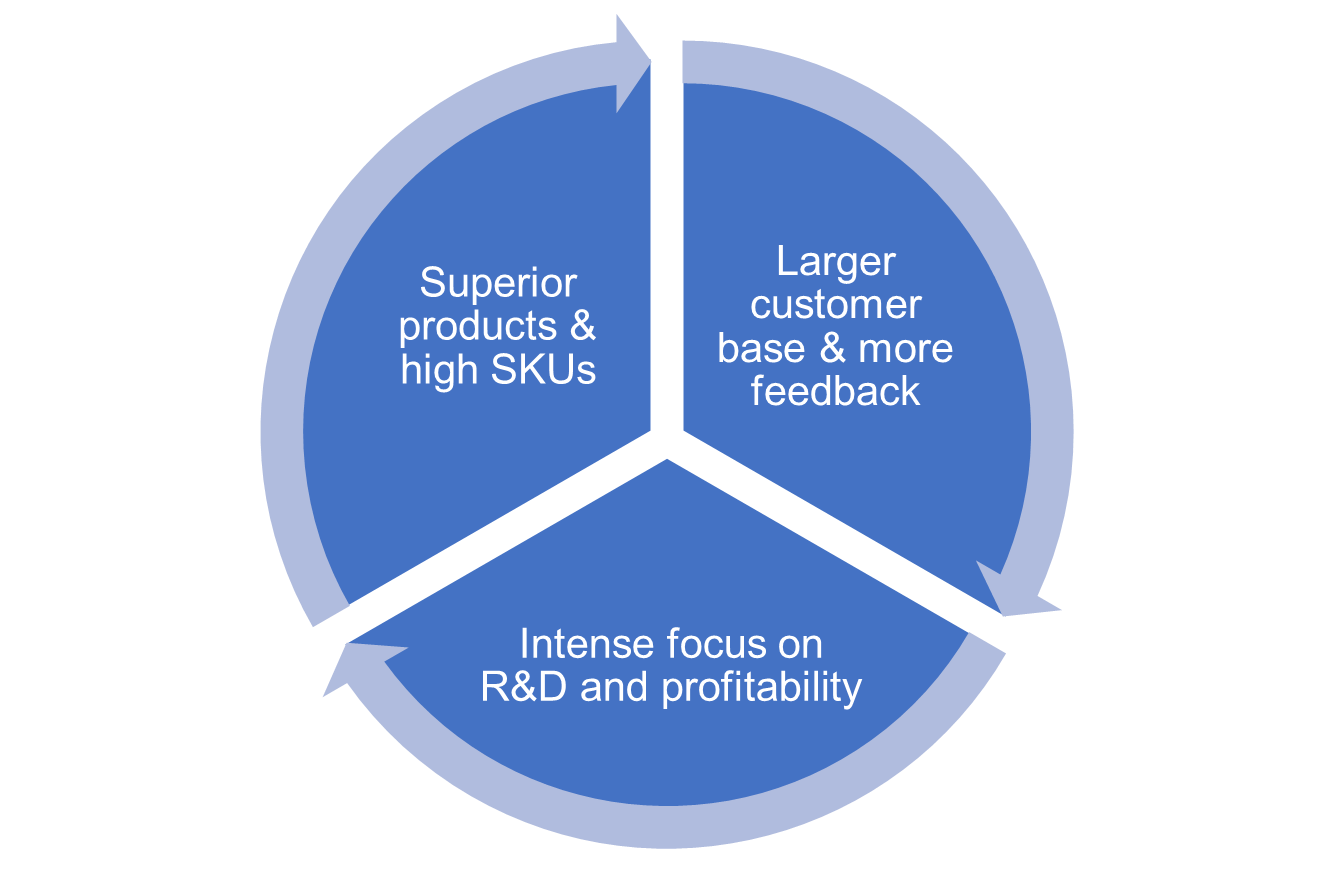

In my opinion, Keyence’s moat can be boiled down to a unique business model — a perfectly calibrated virtuous feedback loop that drives innovation and scale. This results in an incredible money-printing machine that will likely maintain its pole position for the foreseeable future.

1. Product-centric business leads to unparalleled, industry-agnostic products

Two metrics illustrate the product-centric nature of the business: (1) 70% of its products are the world’s / industry’s first, and (2) 10k SKUs.

Keyence’s products are revolutionary and highly versatile which can be adapted across many different industries. Keyence publicly claims that 70% of its products are the world’s / industry’s first, illustrating the product-centric nature of the business. The fact that these products generate 20-30% of revenues annually also goes to show that these products have real world applications, and are not just “high tech toys” which are difficult to commercialize.

Keyence also has warehouses globally with ~10k SKUs to support quick delivery. This positions Keyence as a one-stop-shop, high-quality industrial vision supplier and eases the procurement and replacement process for customers. The fact that these products can be shipped to customers globally within a week is a bonus.

2. Strong, closed feedback loop

This is where the 100% direct sales strategy comes in. Customers generally approach Keyence with a problem in mind rather than a specific product in mind, and Keyence recommends an appropriate solution that solves said problem. More importantly, Keyence’s sales process extends beyond contract signing and product delivery. Its several thousand fleet of sales engineers relentlessly gather feedback from clients, which will be internalized and deeply integrated into the R&D process. With a massive customer base of over 300,000 customers, the impact of this feedback on the R&D process is substantial. This process also forms strong, direct relationships with clients, reinforcing the already strong brand equity.

This direct sales strategy has also led to the rise of two camps of investors: those that think Keyence’s moat is in its “consulting” capability, and those that think it purely lies in its superior products. I believe that it is a combination of the two. As mentioned earlier, Keyence leads the industry in terms of overall product quality, capability and useability. In addition, Keyence prides itself in knowing the customer better than the customer knows itself. Human capital forms a pivotal part of this equation as customers rely on Keyence’s sales engineers to provide the appropriate products to enhance their businesses.

3. Relentless focus on innovation and profitability

Feedback integrated into the R&D process is refined over multiple iterations to finally achieve widespread applicability and profitability — a policy that Keyence strictly adheres to. If the firm is unable to produce products at 80% GPM, Keyence continuously reiterates until it achieves profitability or simply abandons the idea.

Culture

Finally, I wanted to touch on culture for a bit, because it plays a critical role in business excellence (as seen in the rise of those incredible industrial corporations mentioned earlier).

Keyence’s hiring process is rigorous (as with all top-tier corporations in their respective fields). Keyence only hires fresh graduates and rigorously trains every employee from a clean sheet to become specialists in industrial vision. Experienced hires are avoided to prevent the influx of bad habits which erode the firm’s culture.

Perhaps more interestingly, Keyence prefers to hire upper-middle bucket (70th-93rd percentile) candidates. This is because it realized that the top 7% of candidates are most likely to leave for greener pastures; while those in the bottom bucket are just not, well, good enough.

The culture of profitability is manifested even on an individual level. Keyence’s sole KPI is EBIT per employee. Simply put, this keeps every employee laser-focused not only on adding value, but maintaining the company’s industry-leading margins.

Japan FA upcycle will likely return in 2024

The FA sector is a beneficiary of long-term structural themes: (1) Western reshoring of key manufacturing facilities in key end markets; (2) mitigating wage inflation and labor shortage; (3) increasing penetration of IoT / AI content in factories and manufacturing lines.

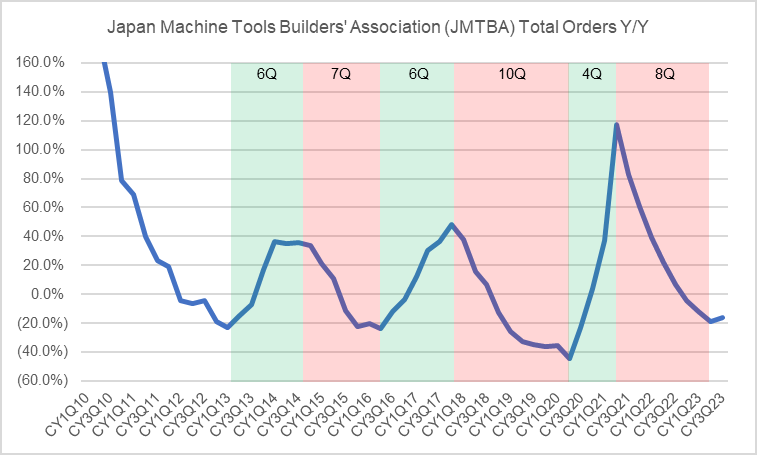

However, the sector is fundamentally cyclical as it is highly levered to the global economy. Products are highly correlated with global capex spending — companies increase capex (and purchase more robots) spending when overall economic health improves and vice versa. As a result, Japanese factory automation (FA) stocks are also incredibly cyclical. These peak-to-trough cycles generally last ~7 quarters.

Unfortunately, 2023 was a lackluster year as a poor macro backdrop dented demand in key end markets, exacerbated by a weaker-than-expected China recovery. Japanese FA stocks have underperformed other sectors as well as the overall Topix index.

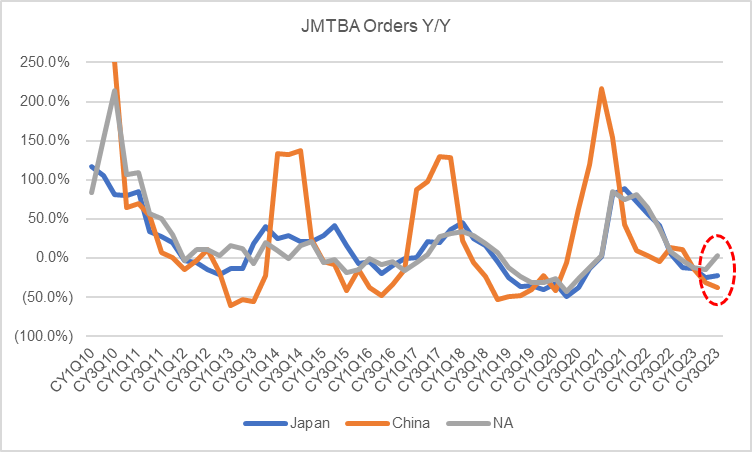

However, I believe the cycle has bottomed and will welcome a new upcycle sometime in 2024 (I estimate ~CY1-2Q24). First, we are beginning to see sequential upticks / slowing declines in JMTBA orders in major markets.

Second, from a macro standpoint, it does seem like a soft landing is the most probable outcome and the market consensus is no longer a recession. The end of the Fed’s hawkish cycle seems near as we see credit markets pricing in rate cuts, evident from the recent ~74bps decline in 10Y yields since peak levels in October this year. We are also beginning to see comforting signs of China’s recovery — the CLI indicator turned positive in April this year and business profits have been improving sequentially. That being said, I see a mild and gradual recovery as policy stimulus rolls in in piecemeal and will likely take a while before we see tangible impacts on companies’ financials.

Third, US reshoring is a meaningful tailwind. Based on current project timelines, US robot orders should inflect sometime in 2Q24 when semiconductor and automotive mega projects begin taking orders / come live. This should bode well for Keyence which has significant exposure to the semiconductor and automotive markets (~35% of revenues).

In essence, the long thesis for Keyence is simple: cyclical bottom in Japan FA meets secular tailwinds, with the recent correction presenting an attractive entry point for the stock.

Debates

There are three main bearish debates I would like to address.

Argument #1: Keyence will find it difficult to compound revenues at 10-15% moving forward amidst greater competition and a weaker China. Japan, US and Europe growth will not be able to support this growth.

I believe growth concerns are overblown due to several reasons. First, China only accounts for ~10% of total revenue. Second, US and Europe’s reshoring in key end markets presents strong opportunities for long-term growth, which is amplified by increasing AI and IoT content in factories and manufacturing lines. Rivals in the West will also likely find it difficult to disrupt Keyence’s leadership position (explained in Argument #3).

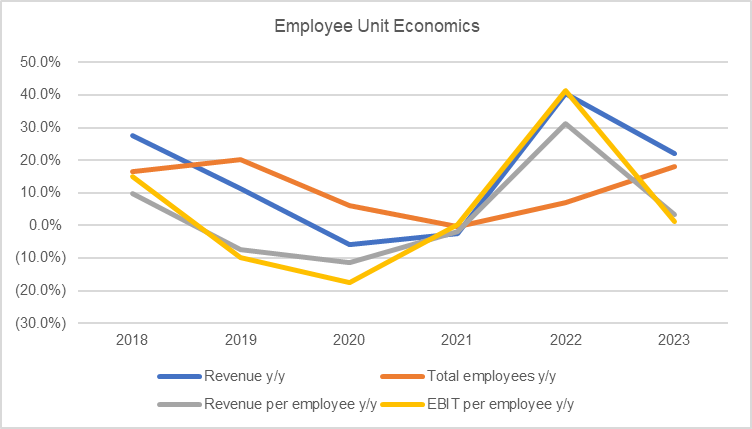

Argument #2: Margins will likely decline moving forward as a result of over-hiring post-Covid to keep up with demand.

Indeed, Keyence’s rapid headcount expansion post-Covid resulted in margin pressure and slight declines in employee unit economics. While this is not ideal, I don’t see this posing material risks to the business in the long term.

First, global expansion has been the firm’s goal since a decade ago and aggressive headcount expansion is inevitable considering the unique business model. Second, I believe the most recent FY2Q24 earnings invalidated this thesis as the company beat investors’ expectations and posted sequential growth in gross and EBIT margins (83% and 52% respectively) amidst a benign demand environment. It is important to note that new hires weigh on margins most since they have to go through rigorous training for one year before they can bring tangible value to the firm. Third, such aggressive hiring is not unprecedented — the firm has done so in the past yet managed to maintain resilient margin levels (sometimes even expanded margins, like in FY16). I believe this is also a strong testament to the firm’s profit-focused culture.

Argument #3: Competition is intensifying as we see a rapid influx of Chinese substitutes. Western rivals also pose a meaningful threat to the business amidst the reshoring theme.

I believe risks are not material because of two reasons: (1) industrial vision is a tough market where scale matters, and (2) factory owners ultimately care about minimizing downtime and hence, product quality.

First, Keyence mainly competes in the ultra high tech precision machinery space, while Chinese alternatives are inferior as they don’t have the technological expertise to produce at scale (and of course, produce profitably). Recently, we have seen multiple Chinese AI startups (Aqrose Technology, XYZ Robotics etc.) gaining some traction amid the AI hype this year. I don’t see this as a big risk due to Keyence’s lead in technology and scale. Take defect detection sensors for example: achieving 98-99% accuracy (which is usually the standard) in defect detection is substantially more difficult than achieving 90% accuracy because it requires an exponentially large dataset of defects to train models and improve accuracy (which in itself doesn’t occur regularly in assembly lines). With >300,000 customers and a clear technology lead, it’s difficult to foresee Keyence facing substantial competitive risks. Additionally, Keyence's first AI product (IV3 Series Vision Sensor) was officially released in 2019, implying that Keyence likely began exploring AI in the early 2010s. Keyence has long been in the “refining” stage rather than the “development” stage in terms of AI.

Second, factory owners (especially blue chip clients) ultimately care about minimizing downtime more than saving costs and are more than willing to pay for higher quality Japanese products than risk downtime which will likely result in greater financial losses.

Valuation

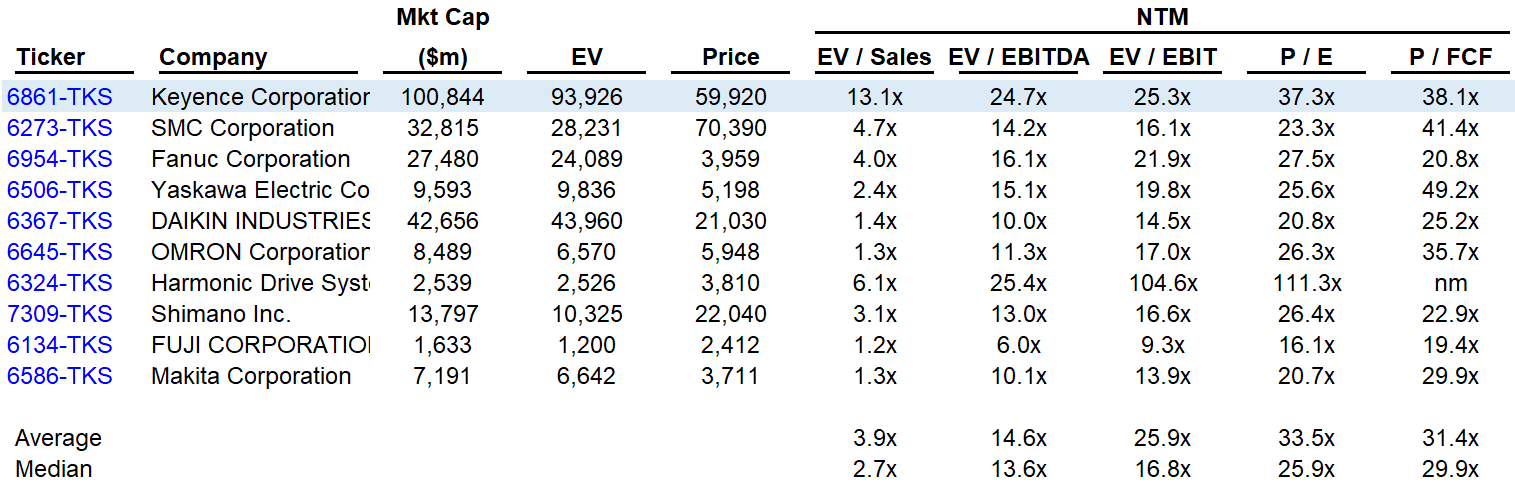

Keyence currently trades at 37x NTM PE, below the 5-year average of 43x. Pitch Keyence to any investor and “expensive” will almost always be the first thing you hear. Keyence’s high multiple creates a significant emotional barrier for investors to commit capital. Nevertheless, investors continued to award Keyence with a significant valuation premium over peers due to its business quality and unparalleled resilience during downcycles. I’d argue that referencing historical valuation is more practical in Keyence’s case.

I believe this stock price reversal has presented investors with a reasonable entry point for a long-term investment in the name. I expect Keyence to reiterate its unique flywheel and maintain its market and margin leadership in the long-term, especially after learning its over-hiring “mistakes” during Covid (again, “mistakes” because it might have well been a conscious one as the company ramps up the global business).

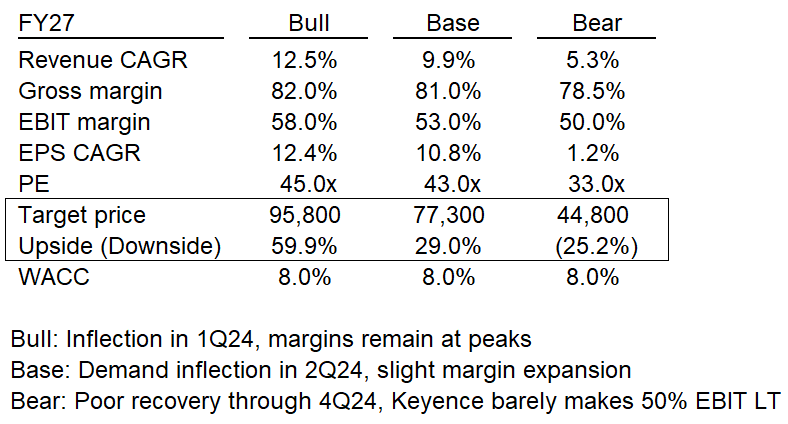

Having compounded revenues historically at +16%, I believe Keyence can continue compounding revenues at a conservative ~10% CAGR through 2028 and slight margin expansion (82% and 55% gross and EBIT margins respectively and achieve JPY 2,165 of EPS. The stock should trade higher near the 5Y average of ~43x. Adding JPY 1,400 FCF per share (~60% FCF conversion in line with historical trends) yields us a JPY 77,300 stock through FY27 (29% upside with 8% WACC / 18% 3Y IRR).

Risks

Given the sector is highly levered to upstream industrial production and manufacturing, the downside risk is that we see delayed recovery through 4Q24 and margins decline due to over-hiring pressure in the near term, and long term revenue growth slows dramatically as Japan and US growth fails to support a weaker China. The stock should trade lower at ~33x NTM PE with +5% revenue CAGR, implying a share price of JPY 44,800 (25% downside). FX headwinds are also not to be ignored as we see a more hawkish BoJ.

Catalysts

Key catalysts: earnings surprises, JMTBA orders improvement, greater / accelerating onshoring capex plans.

Sell-side commentary mentioned that investors are aware of the cycle bottoming out, but are still hesitant as earnings are still declining. I expect earnings to decline further y/y in FY3-4Q24 (CY1-2Q24) as Covid created a high base, though any surprise will be a significant catalyst.

Disclaimer: All views expressed are the sole opinion of the author and should not be interpreted as investment advice. All readers should conduct independent research before making any investment decisions.

Great write-up! Regarding the latest events, I’ve includ the link to your post in the upcoming Friday Roundup.